2015, Mid-Year Market Outlook - JAPAN

For two decades, Japan suffered deflation, stock market stagnation and exorbitantly high debts. Deflation meant that investors did not invest, savers did not save and companies invested anywhere else but in Japan.

That all ended in December 2012 when Shinzo Abe got a second chance at the helm of Japan's government He initiated ground breaking reforms, which became known as ABENOMICS, focusing on how business is done in Japan.

Winning December’s snap election has added power to the PM‘s reforms, resetting values for its business and social culture, and pulling the country out of its deflationary cycle.

The

Central Bank of Japan, BoJ, launches an unprecedented program of vital liquidity,

which rapidly weakens the YEN. Corporate earnings (locally and internationally)

are growing in leaps and bounds and are now strong enough to put pressure on

wages. That has initiated a round of inflation to finally heave Japan away

from the threat of inflation, for good.

Japan’s Economic Health

A

lower Yen is good for Japanese export industries, the most important component of its GDP, and also increases earnings for Japan's international companies.

But imports become dearer. Any resulting price inflation will be welcome! The Japanese leadership has hopes that inflation will help make its debts more manageable: Most of it is owed to local Japanese.

But imports become dearer. Any resulting price inflation will be welcome! The Japanese leadership has hopes that inflation will help make its debts more manageable: Most of it is owed to local Japanese.

Do

the math: If ¥ devalues 30% = ¥ debt 30% less (in USD terms).

Japan imports all its oil, and has been foregoing nuclear power since the the devastating earthquake in Fukushima in 2011. As such, low oil prices are a major bonus for its businesses providing spare cash for companies & consumers alike. Of course, a rise in prices could become a major headwind for the economy.

Japan’s Economic Reforms

The

media dubbed it “Abenomics”, and “Abe’s Master Plan”. These reforms were “designed to jolt

the economy out of suspended animation that has gripped it for more than two

decades.” (Wikipedia wording) It was to be carried by the so-called “Three Arrows” principles, a reference to “fukoku kyohei”, a famous reformation program initiated in 1868, during the MEIJI era, leading to the end of Japan’s feudalistic system.

A few key points were:

A few key points were:

“Enrich

the country.” “Strengthen the army.” “Avoid reliance on foreign loans.”

(The

latter is the principle, why the government borrows from Japanese public rather

than from overseas entities.)

The “Three Arrows”

of Mr Abe:

- Fiscal stimuli: a lower Yen

- quantitative easing: purchasing local bonds

- structural reforms, unleashing economic growth

|

| NIKKEI 225, Source: Chartnexus |

The NIKKEI 225 index is up 68% from October 2012 to Jan 2015, almost 5% flat per month.

|

| YEN/USD over 2 year period; Source: Yahoo!Finance |

YEN

down >30%, from USD 0.81 to USD 1.21, updated 11/7/2015.

Japanese Stock News

Nikkei 225, October 2013 - July 2015

Updated: July 11, 2015

|

| The most interesting period: October 2014 till now; source: Chartnexus. Assessment R. Krieg |

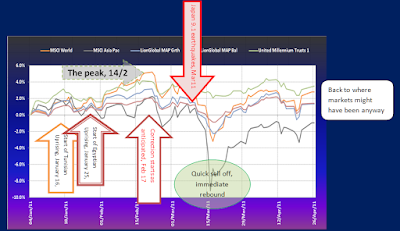

It is worth investigating this chart closely, despite the many indicators, which you may find a little confusing: We want to get a better understanding of where the markets are heading in the coming weeks or months.

The chart starts just before Mr Abe's triumphant victory of the snap election in December 2014. Investors had begun to voice doubts with regards to the sustainability of the reform. National sales figures had suffered when the Sales tax was introduced a little earlier that year. People questioned the government's willingness to invest - substantially - more as it was needed to reinforce economic recovery. Hence the decision for President Abe to call an early election.

From October 2013 through to the most recent peak, June 24, 2015, investors responded very strongly, rushing through the 161.8% (Extended Fibonacci level), which often acts as a final barrier for stock market rallies.

Most recently, the index had its first, more significant correction since 2012. It was a mild correction, - accompanied by some strength in the YEN. The correction stopped at the 61.8% Fibonacci level (end if day close). Very significantly, the volume for stopping the fall was the strongest, suggesting that investor support is huge at this level.

I would suggest that markets will reach higher highs still, before a more protracted consolidation - later this year?

Japanese Fund Performance

|

| Singapore registered Japan Equity funds Source: iFAST Financial, Singapore |

A typical fund performance of <30% tells us that, despite a weakening YEN, fund managers were able to transfer most index gains into SGD gains. That is a laudable result, - and another reason to invest in Japan via investment funds, going forward!

Japan’s DRAWBACKS

History, a reliable guide to the future?

The history of Japan recounts an economy marked by bursts of growth and recessionary lapses. In Japan as well as abroad, many doubt whether the MEIJI success can be repeated. After decades of unsuccessful attempts of escaping the quagmire of deflation, the sustainability of this particular reform is called into question.

In the Western World, there is the saying, “You can lead a horse to the water but you can’t make it drink.” Transliterated into the Japanese context, you could say, “You can ‘reflate’ all you want, and still fail to get the approval of the Japanese public.”

“Old habits die hard”, and it may be especially tough with respect to the Japanese business culture and investor behaviour. Having said that I am more and more inclined to see such reservations as outmoded, stereotypical mumblings, no longer relevant to the Japanese case in the near term.

The doubters have so far been proved wrong. Japan’s economy and stock market has continued to push higher.

Foreign Investor Influence

From an investor point of view, we need to recognise that Japan’s stock market ups and downs coincide with foreign investment flows: when they buy the market rises, when they sell the market falls, often without reflecting acute economic data. The growth in stocks is partly an adjustment to a weakening YEN. Indeed, there has long been an inverse relationship between the currency and the NIKKEI index.New Standards

High returns in Japanese stocks a novelty after decades of deflation, - takes getting used to…

Japan in 2015, Second Half - Expectation

Summary

- Abenomics is the best attempt so far at re-setting a growth trend for Japan’s economy and create benign inflation, deflating its debts.

- The equity rally we have seen I expect to be sustainable, on the basis of future benefits from reforms, but we may need to show patience!

- After a year of boisterous upside in Japanese large caps, we should now look to small caps for exceptional growth.

- The only 'hair in the soup' might be currency fluctuations, mainly from the perspective of foreign investors.

Japan in 2015, Second Half - Bottom line advantages

- Many Japanese companies operate internationally, i.e. earnings come in many currencies.

- A weaker Yen will not necessarily impact their profits, quite the opposite. These companies have learned to hedge the adverse effect of the Yen on their results a long while ago.

- Shinzo Abe has strong support for his reforms. Given ample time, markets will deliver more positive returns.

- The country is a favoured market for foreign investors. They rather invest here, a developed market, than other Asian countries, still ranked as emerging economies.

Comments