No Rate Change - but Stock Markets drop sharply!

Stocks Down Again

By right, no change in interest rates should have resulted in a short rally in stocks and shares. Last Friday, US stocks rallied till lunch time, then tumbled some 200 points, - after the FED announced that rates will stay the same at 0.25%. Was the stock market really reacting to the FED decision? Are punters really that dim to interpret the lack of action as a sign of a secret economic weakness? Well, that is what I hear from the financial whizz guys of the famous networks.If that were so, then why did the German DAX drop 3%(!) all through Friday, closing long before the official announcement came in the US? The Japanese NIKKEI 225 also fell 2% on Friday, and closed 12 hours earlier. Most other markets in the Asia-Pacific had a positive day.

Does that mean the Germans and the Japanese were psychic and knew that the US stocks would go down and reacted preemptively, - while the others only "cared" for their own little markets? Or - did the worry in Japan and Germany infect the minds of US investors?

It is always quite astonishing to listen to the kind of laboured associations being conjured up as to who caused what and why. If it makes you smile, then count yourself lucky. There are plenty of wretches who - having relied on the forecasted rally - counted only losses on Friday night. And frankly, they don't care much for the explanations.

Cause And Effect

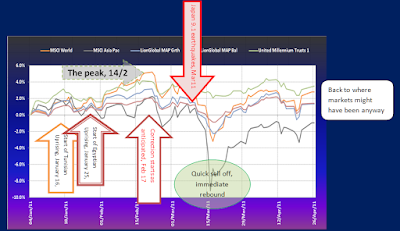

Looking for a logical cause-and-effect kind of reasoning is not what I proposed, when I wrote about the possible outcomes of last week's FED meeting. Today, I feel emboldened to claim victory for the stock market cycles. These cycles do work over various periods and an end is often indicated by a low. If our research is correct then at present there are several ending phases of cycles culminating, putting extra selling pressure on investors. I say "our" because I am not the only one in this still largely undervalued, under-researched and even misunderstood field of expertise.

Cycles Count

Cycles don't just influence financial markets. They affect people in general.

One particular cycle worth investigating is the one that started with the Tunisian trader, Mohamed Bouazizi, who burned himself in December 2010. It started a rebellion, which has become known as the ARAB SPRING. It relatively quickly spread to many other islamic countries, and many people were enthusiastic about this so-called new democratic conscientiousness. But even in 2010, I warned in my blog that after an Arab "spring", a hot summer follows and when it does, the democratic cause would be tested and counter forces could tip the euphoric mood, resulting in a major setback.

Here we are five years later, faced with a disastrous situation in Syria, a new terrorist threat in the form of ISIS, a mounting refugee crisis for Europe and many confused politicians as to how this and everything else Middle Eastern could possibly be resolved.

Why?

The biggest hangup for people, trying to learn about cycles, is the often obscured or "missing" link between a causal trigger and the resulting effect. The reason for that is that cycles come in multiples. For instance - the market in the US is at a different cycle phase than - say - China, or Europe. In fact the breakdown continues into individual countries, industries and - long, medium and short time frames, thus complicating matters.

For that reason, we, "market timers" and trend followers, tend to limit ourselves to the big, voluminous trends that last longer than a month. Waiting for this kind of move forces us to consider the impact of cycles that really matter, i.e. cycles that seriously impact on your gains and invested capital in the medium term.

Losses Ahead!

As I said a week ago, (and earlier) stocks and shares have entered a bear phase when losses are imminent, losses that can easily wipe out 10-15% of your investment in the short term. Taking into account the time frame for this correction, I would not be surprised to see losses grow to 25% by next February.

When stock markets correct, often bond markets will see gains, but only the safe bonds, - not the high yield, or junk bonds. So far, the bond funds I watch seem to adhere to this premise. Whether the inverse relationship between bonds and stocks continues throughout this long correction remains to be seen. It is possible that bond investors panic, too when sharp currency fluctuations further distort the outlook. Yes, currencies are another asset class that will be very volatile this coming winter.

A "Silver Lining"

Precious metals are presently the beneficiaries of the correction. Its prices have gone up considerably and due to rally further. However, I would like to caution those who already see a new super rally unfolding. By mid October, the pendulum could already swing the other way again. Stake a sensible amount that does ruin you if the markets turn again. For a Super Rally in gold we may need to wait till 2016. I know it's not far, but I am always wary of buying an asset where the downside potential is almost as large as the expected upside. That is why I described gold as a silver lining, not a must-have asset at this point.

Concluding

To expect logical reasoning and time-tested parameters to drive the market is a thankless task. As it was in 2010 and 2012, market corrections come abruptly and leave little time to respond. This time, at least the cycle researchers told about this one coming. Don't take it lightly and - if in October there are a few weeks of rebound - don't think Father Christmas has come early. Indeed, I expect the Santa Rally to go down badly. Maybe, if you are clever and experienced enough, you can short the markets? I find it a bit daunting.

Comments