2015 Mid-Year Financial Market Report: Intro-Overview

Where needed, the June update is in RED and highlighted. The rest is a repeat of the original text as created from December 2014 to January 2015. I am happy that so far, few of last year's statements required correcting.

- PART ONE -

A common desire in 2015

Investment returns are the lifeblood of any investor, and

indeed, the investment industry at large; - the more, the better. BIG BUSINESS

loves low-risk, passive returns. But, with interest rates near 0%, finding worthwhile risk adjusted returns is like getting blood out of a stone!

If there is one theme in 2015 that is pressing on every

investor’s mind it is the lack of risk free returns. A belligerent race for returns ensues,

riskier and often more frustrating than it has been in a long while. As we are waiting for the US Federal Reserve to proceed with

their first interest rate hike in more than 10 years, we should check what kind

of risks this will unleash: Indeed, who can confidently predict the levels of

risk and their impact? All asset classes will face re-pricing as a result. The

kind of fallout we will actually experience cannot be statistically demarcated.

And so we, hoping for the best as humans do, we entered 2015.

The hunt for return in first half of 2015 has been controversial and surprising - like most years. Now, as is customary, many questions arise:

- Where are the easiest & least risky return to be had?

- What drives markets - and investors - in their pursuit of gain, around the world today?

- How can we diversify optimally without diluting our chances for returns? How do we position a portfolio in moving markets?

- What kind of strategy is most suited to this investment environment? Where does asset allocation fit in?

- What’s hot and what’s not for a next few months?

As investors, we expect superlative returns!

We have entered the race in January with trepidation. Conflicting

dynamics muddy the outlook. For seven years, markets enjoyed abundant

liquidity, a FED prescribed medicine to get the US (and the rest of the world)

out of the 2008 Great Financial Crisis. This liquidity program has ceased last

year and this year, everyone talks about the first interest rate increases in

the US. Simply put, this will make the US dollar rise versus other world

currencies.

In contrast, the European Central Bank (ECB) and the Japan

Central Bank (JCB) have embarked on their most ambitious quantitative easing measures,

the ECB in May this year, and the JCB in November 2013. As a result, both the Euro (EUR) and the YEN

have dropped sharply against the USD. This, I observe, stirs up above average movement in the financial markets, i.e. asset rotation. It happens without due consideration of fundamental economic data. USD investors with their

strong dollar buy and invest overseas. Many asset valuations are undergoing major adjustments as we speak. Just look at prices of precious metals, oil and other commodities.

Emerging market currencies are under pressure and globally, central

banks are reducing interest rates and apply other fiscal measures to stem the threat of inflation or indeed, deflation prevalent in Europe.

This battle is accompanied by a persistently low oil price

environment. It is

said to help the global economic recovery, makes it

cheaper to transport goods and people. Lower energy bills create cost savings,

too. But we tend to overlook that oil producing economies suffer a massive drop in income, affecting national GDPs and local

businesses. At some point this will also feed into the global economy and cause ripples in financial markets.

Review

How did we get to where we are?

A good place to start: The US equity market.

Investors outside of the US can question our preoccupation

with US affairs. But, investors, anywhere in the world, look to the US for clues on trends, &

information, hoping to obtain guidance and direction for their next trade. It has

the world’s largest investor base, trading the largest volumes: these guys move

markets. USA stocks, shares, bonds, and other investable assets are popular and readily

accessible! The analytical tools and trading platforms are highly evolved. Data is

accurate, timely, detailed, and comprehensive. News channels cover all US markets

throughout. And, the USD is the most recognised reference currency: apart from

world trades, the majority of investor money is in USD, even in Asia.

The S&P 500, a 20-Year View

|

| Source: Chartnexus - own research parameters |

S&P 500: index in March 2009 is… as low as in 1995, and

lower even than 2002, the bottom after the dot.com bubble burst! That is the

view for the USD investor. The overall picture tells us that stock markets don’t

always go up, AND the drop from the peak is usually sharper and shorter than

the rise! As we have reached the highest points in the US, the mood among investors has changed: there are those who enough is enough, we sell now and wait for the turnaround, and there are others, who consider it the "safest point" of entry for them.

The picture for those who think in other currencies will be quite different. They need to take account of the movement of their

reference currency versus the USD. Let’s

look at how an investor, with Singapore dollars as a reference, sees valuations unfold: The SGD gained strength against the USD for most part from 2002 till now.

He asks: “Why is my SGD portfolio performing so differently

from US stock market performance?! Why did I not see the gains I ‘see’ in the

US indices?”

My Singapore Dollar Investment: A 12-Year View

In the chart above, we see the SGD appreciating by 33%

against the US dollar over 12 years. Therefore, any returns in the S&P 500

(or other USD asset) over that period was countered by a 33% drop in the USD.

Why did the USD lose so much buying power? Quantitative

easing by the Federal Reserve, introduced in 2008, resulted in interest rates

dropping to near 0%. This means, bank deposits and investment grade bonds yield almost nothing! In search of yield, USD cash flows abroad,

into Asian equity, leading to non-US equity outperforming US equities from 2009-2012.

A Dollar Swap …12 Years ago

Had an investor converted his Singapore Dollar into US Dollar in

2003, when the USD/SGD ratio was around S$1.80, and held it till end of 2013, he would have suffered a painful loss of buying power!

By April 2014, the USD/SGD ratio was S$1.20, i.e. a loss of some 33%.

How did the dollar slide affect SGD investment?

Let’s take

another look at investment returns in equities, over a shorter time frame:

The S&P 500, 10-Year Performance Summary

The figures in my

calculations are rounded. The principle message counts, "how currencies distort our perception of real return", not the figures.

- Ten years ago, the S&P 500 stood at 900 points.

- It rose to near 2000 points at the end of 2014.

- This represents a gain of [900 to 2000 =] 1100 points or 110%, based on USD valuations.

·

In SGD terms, we need to convert the end result

(2000 points) to SGD: 2000 x 66% = 1333. We can now make the same performance

calculation: 900 to 1333 points = 433 points, representing just under 50% gain.

We can therefore confidently state that fluctuating

currencies distort ‘real or realised’ returns.

The REAL RATE OF RETURN is a function of

- invested currency, underlying asset price development, currency volatility, & time.

To showcase the effects, let us look at two more charts of

global indices over a 5-year and a 1-year period.

Global Equity Indices; annualised returns, in SGD

Performances don’t surprise with respect to US indices, but the rest of the world certainly did. Most notably, performances are anything but correlated. Regional events dictate the outcome, like the super returns in India, Thailand, Japan, or the disastrous ones in Russia and the emerging market oil producers.Over 5-year term (annualised):

Best with +17.8%: NASDAQ 100

Worst with -11.14%: Russian RTS

Over 1-year term:

Best with 30.12%: Mumbai SENSEX

Worst with -45.19%: Russian RTS

Now let’s look how much of that performance translates into actual returns in mutual funds (unit & investment trusts), the core investment

tool for many investors.

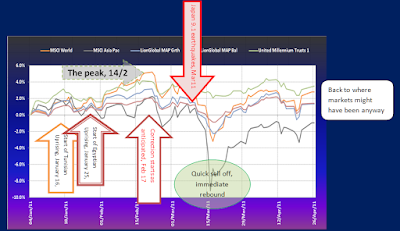

Singapore registered Fund Performances in 2014

Unit Trusts chart: explained

In the chart, we use “average fund performance” figures,

so-called FSM indices, sourced through the iFAST platform, avoiding selective bias. All fund prices are in converted to SGD prices.

Coloured Chart selections:

1st quarter: increasingly volatile;

mid-year: positive returns;

4th quarter: highly volatile.

Average

global fund return (in Singapore dollars) ≈ 3-6 %, excluding fees (initial charge, platform and

advisory fees).

Who is to blame for the poor performance of funds and global portfolio strategies?

Here is my personal verdict: It is the result of

- unsuitable and/or untimely asset selection (= fund concepts, prescribed strategies, rigid investment allocation structures, and not necessarily just bad management);

- currency fluctuations;

- large withdrawals by punters. Outflow from unit trusts was well above average in 2014.

- Charges for fund management, advisors, trading, hedging, - all of which are still much higher in Asia than in Europe or the US.

- All of the above and in that order!

Reality Check

To put it into perspective, please remember:

- Indices do not include costs for acquisition, management, account charges or trading we may have incurred in real life.

- Funds and ETFs do not necessarily carry all the assets contained in an index or benchmark.

- Collective investments (=funds) levy fund management, and at times performance, fees Platforms charge platform and custodial fees. Initial, switching and advisory fees further reduce overall performance.

It is not all bad:

- The RK Traffic Lights system (RKTL) (a proprietary fund analysis system for Singapore registered funds) lists – and recommends – only the best funds in their peer group (affirmed and proven historically), taking into account long term indicators and short term momentum.

- RKTL funds performed better than average.

- The internal costs of funds are carefully screened to deliver better value for money.

- Good fund managers may indeed outperform their index / chosen sector.

- Some funds can generate extra returns by investing in securities not included in the index.

- the RKTL provides asset allocation strategy, too, so you will know when and where to invest, and when to make changes.

Finally

- The Realised Return for the investor = quoted fund return, take away transaction fees

- Performance is relative & subject to (mental) distortions.

- Correlation among countries, sector or asset class varies leading to performance divergence, especially long-term.

- Following the Great Financial Crisis in 2008, it is much tougher to choose the next winner.

- Fiscal measures and political decrees greatly influence financial markets and investor behaviour.

Essential for success: the right tools and asset class

focus, followed by regular reviews, and timely rebalancing.

Comments