Global Markets - A few days in the RED - and then?

Many times I have outlined views on the main driver of global capital markets, the indices in the US, simply because of their close correlation to stock market affairs in Asia.

Today, I want to comment on issues closer to home. In our SC Monthly Market Outlook, published in the first week of November, I commented on the STI, drawing a few directional arrows into the topical chart to outline the likely path for the coming weeks.

The STI has already reached heights of over 3,300. My research suggests that advancing from this level will require another QE because QE2 has extended gains beyond forecasted levels. The chart on the right shows the index right up the announcement of QE2.

Respite came promptly in recent days, with a chance for overbought conditions to normalise.

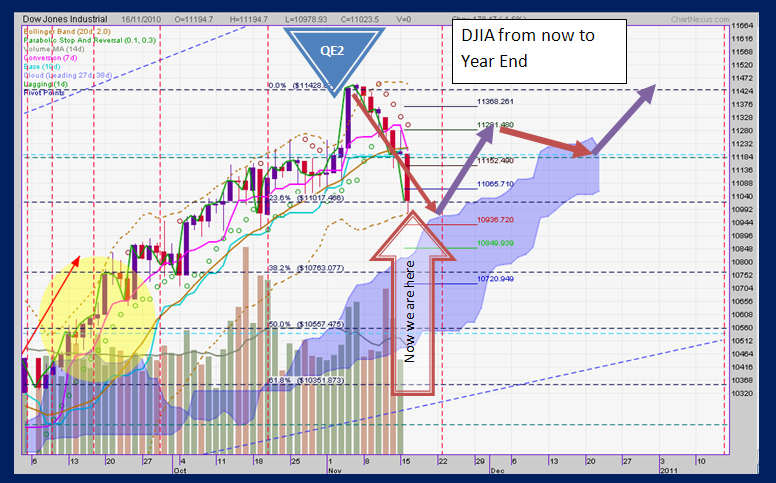

On the right is the updated chart including the last few days' action.The sequence of red arrows start on the announcement of QE2 (red triangle). The big orange arrow points to where we are now.  Nice enough, the index closely follows the arrow I have drawn! Thankfully, today is a public holiday so we have some extra time (and one more overnight action in the US markets) to contemplate whether Asian indices should "follow" the lead from the US markets SOUTH, - or whether our markets have already done all the necessary correcting, and it was in the US that the last shoe dropped (my preferred conclusion)!

Nice enough, the index closely follows the arrow I have drawn! Thankfully, today is a public holiday so we have some extra time (and one more overnight action in the US markets) to contemplate whether Asian indices should "follow" the lead from the US markets SOUTH, - or whether our markets have already done all the necessary correcting, and it was in the US that the last shoe dropped (my preferred conclusion)!

Nice enough, the index closely follows the arrow I have drawn! Thankfully, today is a public holiday so we have some extra time (and one more overnight action in the US markets) to contemplate whether Asian indices should "follow" the lead from the US markets SOUTH, - or whether our markets have already done all the necessary correcting, and it was in the US that the last shoe dropped (my preferred conclusion)!

Nice enough, the index closely follows the arrow I have drawn! Thankfully, today is a public holiday so we have some extra time (and one more overnight action in the US markets) to contemplate whether Asian indices should "follow" the lead from the US markets SOUTH, - or whether our markets have already done all the necessary correcting, and it was in the US that the last shoe dropped (my preferred conclusion)!

Was it the last "shoe"? A big down day like yesterday is often followed by an ending pattern and then the rebound comes. The present advance is clearly confined by Fibonacci relationships and time lines, thus supporting the near-term outlook in the best possible terms. Again, forecast starts at QE2 (this time a blue triangle) The orange arrow again points to the most current decline. Whether the next steps pan out this way depends on how the next purchase by the FED is received. By buying daily (but probably not much last night), future volatility is likely to be kept in check.

Bond Disappointment

It has been a miserable few weeks for bond holders. Neither QE2, nor the notion of higher interest rates sooner rather than later helped overall sentiment. Worse still, investors saw only rising equity markets ("I am missing out"), and even when markets turned down, bond prices kept falling. It is rather disconcerting when a well planned strategy is waylaid by a breakdown of the normal interdependency between equity and bonds we relied on for its success. Maybe the most recent pullback in stocks offers a few extra points. But wait around we won't. Our portfolios are now switching out of bonds, anyway.

The USD has appreciated and the equity outlook is now seen as less certain in the short term, just the right climate for a contrary action: Time to buy into the markets, I say. Bother with the PIIGS states in Europe? Well, consider the latest trouble in Ireland just another act in the ongoing, well defined drama that will probably be dealt with as pragmatically as the more grievous Greek bailout. There are 5 European piglets in a similar dilemma. Only a multiple default event would upset the current game plan there.

The USD has appreciated and the equity outlook is now seen as less certain in the short term, just the right climate for a contrary action: Time to buy into the markets, I say. Bother with the PIIGS states in Europe? Well, consider the latest trouble in Ireland just another act in the ongoing, well defined drama that will probably be dealt with as pragmatically as the more grievous Greek bailout. There are 5 European piglets in a similar dilemma. Only a multiple default event would upset the current game plan there.

The next move in the capital markets will not be pro-bonds, but pro asset inflation. This time, the planned interventionist action is even more concerted than in April 2009, and so will the outcome of stock prices be.

Comments